Corporate Presentation

AstraZeneca Pharma India

Limited (AZPIL)

May 07, 2013

2

Disclaimer

2

This presentation by AstraZeneca Pharma India Limited (the “Company”) is solely for your information and may not be taken away, distributed, reproduced, or

redistributed or passed on, directly or indirectly, to any other person (whether within or outside your organization or firm) or published in whole or in part, for any

purpose by recipients directly or indirectly to any other person. By accessing this presentation, you are agreeing to be bound by the trailing restrictions.

This presentation does not constitute an offer or invitation to purchase or subscribe for any securities in any jurisdiction, including the United States. No part of it

should form the basis of or be relied upon in connection with any investment decision or any contract or commitment to purchase or subscribe for any securities.

None of our securities may be offered or sold in the United States without registration under the U.S. Securities Act of 1933, as amended. This presentation is not

intended to be a prospectus (as defined under the Companies Act, 1956) or an offer document under the Securities and Exchange Board of India (Issue of Capital

and Disclosure Requirements) Regulations, 2009 as amended.

Further, in order, among other things, to utilise the 'safe harbour' provisions of the US Private Securities Litigation Reform Act 1995, we are specifically providing the

following cautionary statement: This presentation may contain certain statements with respect to the operations, performance and financial condition of the

Company and/or AstraZeneca Plc, which may be construed as forward-looking statements. Although we believe our expectations are based on reasonable

assumptions, any forward-looking statements, by their very nature, involve risks and uncertainties and may be influenced by factors that could cause actual

outcomes and results to be materially different from those predicted. The forward looking statements, if any, reflect knowledge and information available at the date

of preparation of this presentation and the Company undertakes no obligation to update these forward-looking statements. Important factors that could cause actual

results to differ materially from those contained in forward-looking statements, if any, certain of which may be beyond our control, include, among other things: the

loss or expiration of patents, marketing exclusivity or trademarks, or the risk of failure to obtain patent protection; the risk of substantial adverse litigation/government

investigation claims and insufficient insurance coverage; exchange rate fluctuations; the risk that R&D will not yield new products that achieve commercial success;

the risk that strategic alliances and acquisitions will be unsuccessful; the impact of competition, price controls and price reductions; taxation risks; the risk of

substantial product liability claims; the impact of any failure by third parties to supply materials or services; the risk of failure to manage a crisis; the risk of delay to

new product launches; the difficulties of obtaining and maintaining regulatory approvals for products; the risk of failure to observe ongoing regulatory oversight; the

risk that new products do not perform as we expect; the risk of environmental liabilities; the risks associated with conducting business in emerging markets; the risk

of reputational damage; the risk of product counterfeiting; the risk of failure to successfully implement planned cost reduction measures through productivity

initiatives and restructuring programmes; the risk that regulatory approval processes for biosimilars could have an adverse effect on future commercial prospects;

and the impact of increasing implementation and enforcement of more stringent anti-bribery and anti-corruption legislation. Nothing in this presentation should be

construed as a profit forecast.

This presentation is for general information purposes only, without regard to any specific objectives, financial situations or informational needs of any particular

person. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness

of the information or opinions which may be contained in this presentation. Such information and opinions are in all events not current after the date of this

presentation. The Company may alter, modify or otherwise change in any manner the content of this presentation, without obligation to notify any person of such

change or changes.

3

Overview

3

1

2

3

AstraZeneca Plc Overview

AZPIL: Business Overview

AZPIL: Key Highlights

4

Overview

4

1 AstraZeneca Plc Overview

5

AstraZeneca Plc: Business Overview

5

Global research and innovation driven Integrated

biopharmaceutical Company focusing on the discovery,

development & commercialization of prescription

medicines in 3 core therapeutic areas namely Cardio-

metabolism, Oncology and Respiratory & Inflammation,

and also present in the therapeutic areas of

Neuroscience and Infection & Vaccines, on an

opportunity-driven basis

Formed in April 1999 through the merger of Astra AB of

Sweden and Zeneca Group Plc of UK

Ranks among the top 10 pharmaceutical companies

globally with CY2012 revenues of $ 27.97 bn and

CY2012 core operating profits of $ 10.43 bn, with a

market capitalization of $ 64.91 bn (as on May 03, 2013)

Sixth fastest growing MNC pharmaceutical company

across emerging markets (Emerging Markets revenue

was up 9% in Q1CY13 vis-a-vis Q1CY12 (CER))

Operations in more than 100 nations globally and

employs around 51,700 employees worldwide

Global Sales (Geographical Split)

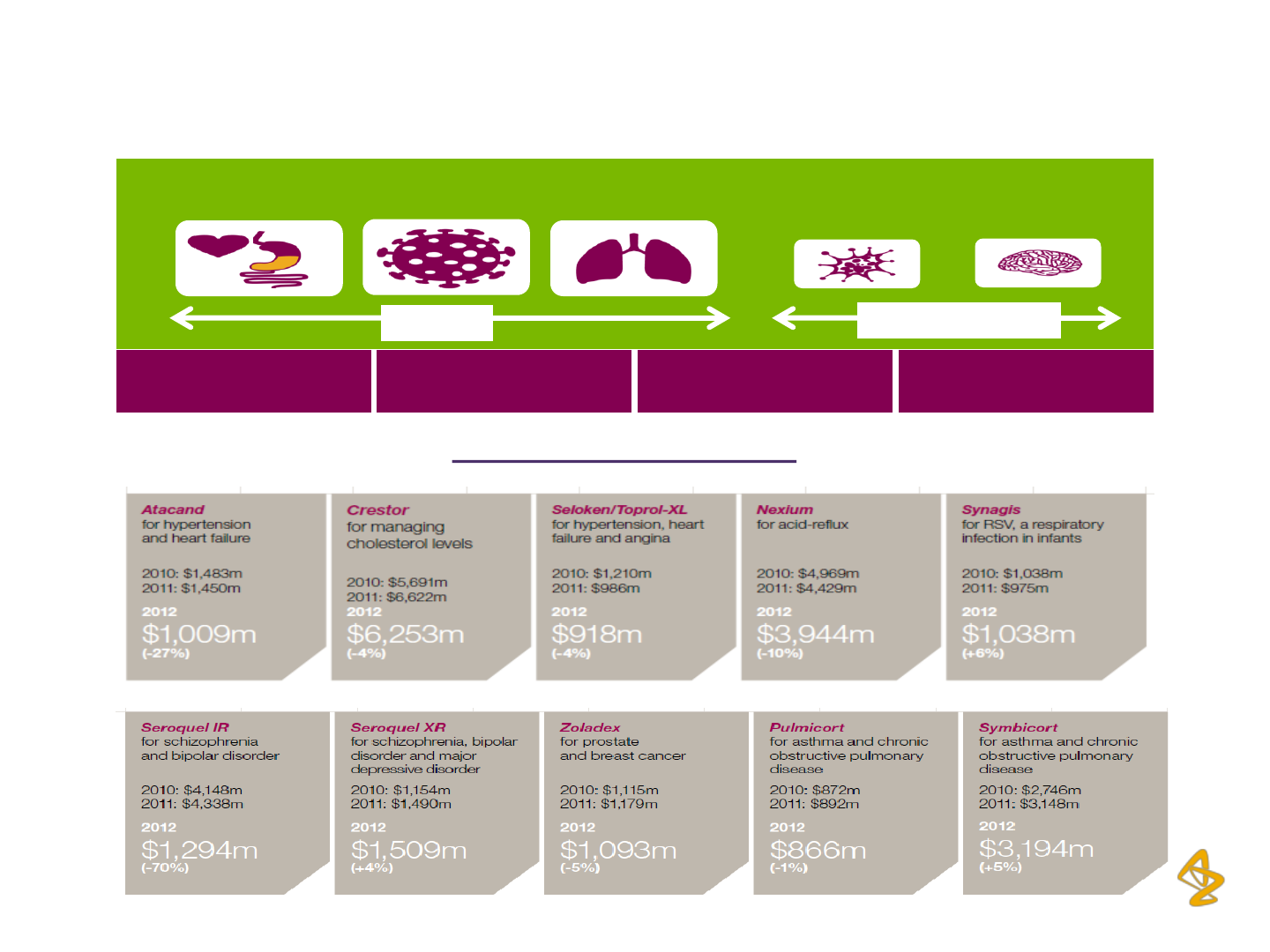

Strong Brand Portfolio

8 brands with Sales of more than $1billion in 2012

Source: AstraZeneca Plc, Annual Reports and Investor

Presentations

6

AstraZeneca Plc: Vision & Identified Growth

Platforms

6

To be a global biopharmaceutical business delivering great medicines to patients through innovative science

and excellence in development and commercialization

A science-led, innovation strategy

Broad R&D platform focused on 3 core Therapeutic Areas (TAs)

Balanced portfolio of specialty and primary care products

Global commercial presence, with strength in emerging markets

Vision

Identified Growth Platforms

1. Cardiovascular / Brilinta

2. Diabetes

3. Emerging Markets

4. Respiratory

5. Japan

Source: AstraZeneca Plc, Annual Reports and Investor Presentations

AstraZeneca Plc: Focus on distinctive science

in 3 core therapy areas

7

Key Products and Brands

Cardiovascular

Neuroscience

Gastrointestinal Infection

Respiratory & Inflammation Oncology

Neuroscience

Infection &

Vaccines

Cardio- Metabolism

Respiratory/

inflammation

Core TAs

Oncology

Opportunity-Driven

Protein

engineering

Biologics

Small

Molecules

Immuno-therapies

Source: AstraZeneca Plc, Annual Reports and Investor Presentations

8

AstraZeneca Plc: R&D Overview

Over $4.5 billion investment in R&D in CY2012, with

nearly 9,800 employees working in R&D Division

R&D presence in 10 principal R&D centres in six

countries (including one in India), covering both small

molecules and biologics

Strong and growing R&D presence in Asia

R&D efforts focused on three key therapy areas: Cardio-

metabolism, Oncology and Respiratory & Inflammation;

opportunistic R&D investment in Infection & Vaccines

and Neuroscience

Collaborations with different companies globally which

has further augmented the current R&D pipeline, with

approximately 40% being sourced externally

Setting up strategic research and development centers

in the U.K., U.S. and Sweden to improve pipeline

productivity and to aide in establishing AstraZeneca as a

global leader in biopharmaceutical innovation

Key Strategic Centers for R&D activities

Gaithersburg

Primary location for

Company's biologics

activities, and Global

Medicines;

Development activities

for small and large

molecules

Global centre for

research and

development, with a

primary focus on small

molecules

Mölndal

Cambridge

Note: These three strategic sites will be supported by other

existing AstraZeneca facilities around the world, including

Boston, Massachusetts, US which will continue to be a centre

for research and development, with a primary focus on small

molecules

Set up of New site in

Cambridge with close

proximity to University of

Cambridge and world

class UK Bioscience

community.

Source: AstraZeneca Plc, Annual Reports and Investor Presentations

Phase I

26 NMEs

Phase II

21 NMEs

Phase III / Registration

6 NMEs

moxetumomab*

MEDI0639*

AZD2014

MEDI3617* AZD1208

MEDI-565* AZD9150

volitinib*

MEDI6469*

MEDI4736*

AZD8330*

MEDI4212

AZD8848*

AZD7594*

AZD5363*

AZD3293*

ATM AVI

AZD1446*

MEDI2070*

MEDI9929*

MEDI5872*

MEDI5117

MEDI-557

MEDI-559

MEDI-550

MEDI-551*

tremelimumab

AZD4547

MEDI-573* selumetinib*

benralizumab* AZD5069

Olaparib

#

mavrilimumab*

MEDI8968*

AZD2115*

sifalimumab* AZD1722*

tralokinumab

AZD6765

AZD5423*

MEDI7183*

AZD3241

AZD5847

AZD5213

brodalumab* lesinurad

metreleptin*

naloxegol*

fostamatinib*

CAZ AVI*

Legend

Oncology

R&I

CVMD

Neuroscience

Infection

Large Molecules Small Molecules Large Molecules Small Molecules Large Molecules Small Molecules

AZD7624

MEDI-546*

Changes since FY2012: MEDI-575 and MEDI7814 discontinued; AZD3480 returned to Targacept; AZD7624 progressed into Phase I; and

AZD1722 progressed into Phase II.

Note: CXL status is pending an FDA discussion.

Parallel indications not shown above: fostamatinib (haematological malignancies); MEDI-551 (multiple sclerosis); and tralokinumab

(ulcerative colitis).

* Partnered product

AstraZeneca Plc: Robust R&D Pipeline…

10

Source: AstraZeneca Plc, Annual Reports and Investor Presentations

#

Decision to accelerate Olaparib to Phase III,

and committed to EU filing in 2013

2012 2013E 2016E

11

…With Impressive Phase III Portfolio…

11

Anticipate ~5-7 NME Phase III Starts

2013 2014

benralizumab

asthma

AZD6765

depression

ATM AVI

serious infections

Olaparib

#

solid tumours

sifalimumab/MEDI-546

systemic lupus erythematosus

AZD4547

gastric cancer

moxetumomab pasudotox

hairy cell leukaemia

mavrilimumab

rheumatoid arthritis

AZD5069

asthma

selumetinib

non-small cell lung cancer

MEDI-551

haematological malignancies

tralokinumab

asthma

In 2013 – 2014, AstraZeneca Plc anticipates ~5 – 7

NME Phase III starts

10 potential NME submission opportunities between

now and 2016

By 2016, AstraZeneca Plc will reach its target

volume in Phase III and Registrations

Phase III & Registration NME pipeline volume (#)

Near Term

6

8

9 - 10

Source: AstraZeneca Plc, Annual Reports and Investor Presentations

#

Decision to accelerate Olaparib to Phase III, and committed to EU filing in 2013

12

…Providing Attractive growth opportunities

Over

$ 1Bn

AZD5069 benralizumab Brodalumab^ (2015)

fostamatinib (2013) lesinurad (2014)

MEDI-551 naloxegol (2013)

Olaparib

#

(2013)

selumetinib

sifalimumab / MEDI-546

tralokinumab

Upto

$ 1Bn

AZD4547 ATM AVI CAZ AVI (2014)

AZD6765 metreleptin (2013)

mavrilimumab Moxetumomab

Low Medium

High

Phase III

Phase II

Phase I

Legend

Potential peak year sales for

New Medicines

KEY: (20xx) Year in brackets represents planned year of regulatory submission

^Gross revenue – not AZ share for Brodalumab

Peak Year Sales (PYS) includes lifecycle management opportunities

Strength of evidence to date

Source: AstraZeneca Plc, Annual Reports and Investor Presentations

#

Decision to accelerate Olaparib to Phase III,

and committed to EU filing in 2013

13

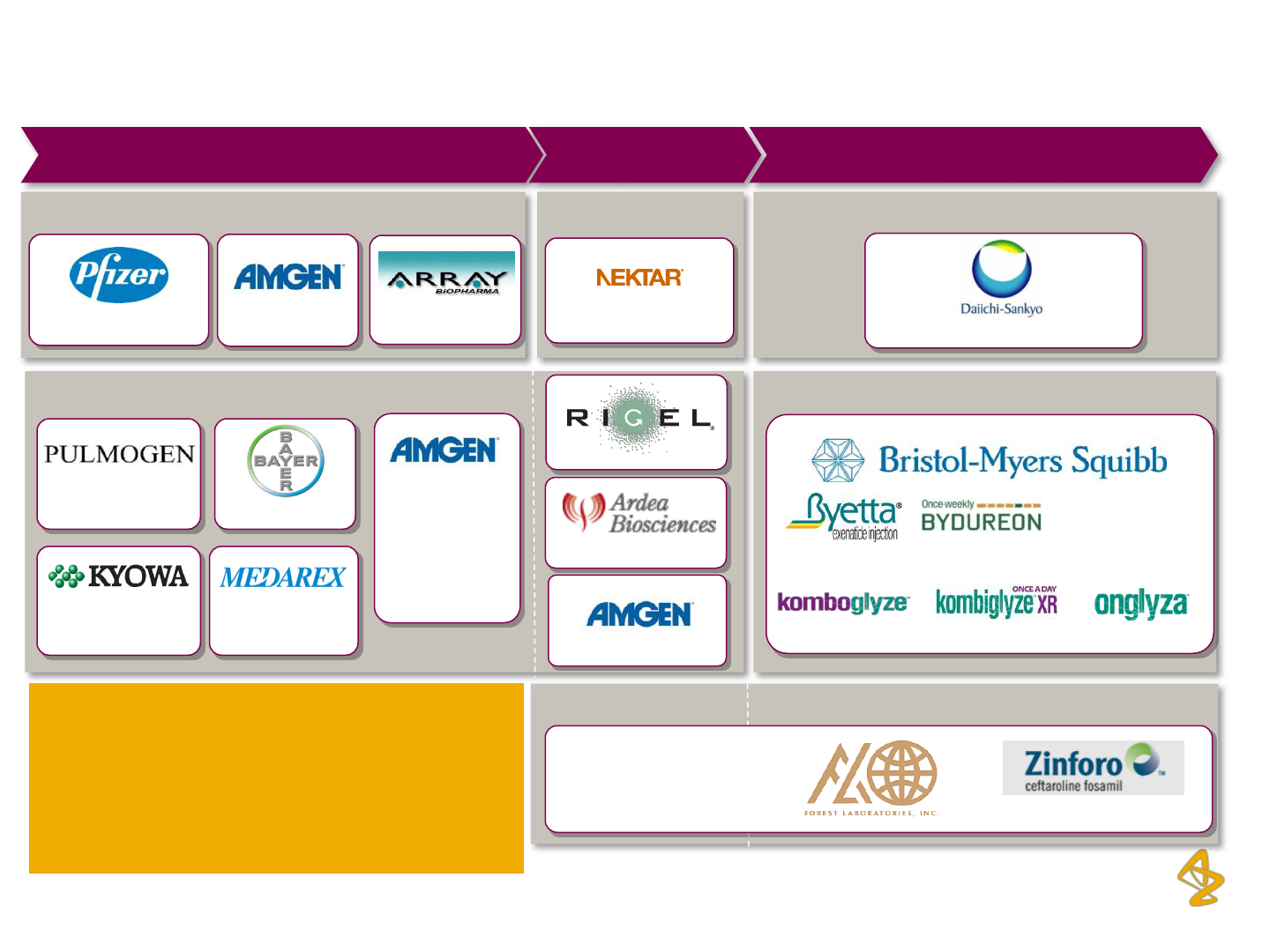

AstraZeneca Plc: Expanding partnership pipeline

13

Oncology CNS

Diabetes

Infection

Respiratory & Inflammation

Oncology

Benralizumab

Lesinurad

Fostamatinib

AZD5423

Tremelimumab

Phase II

Phase III/

Registration

Launched/

Approved (2012)

Selumetinib

AZD2115

AMG139

AMG157

AMG181

AMG557

MEDI-8968

Sifalimumab

MEDI-546

RANMARK (Japan)

CAZ AVI

MEDI-575

Brodalumab

Naloxegol

EU

FORXIGA

Source: AstraZeneca Plc, Annual Reports and Investor Presentations

AstraZeneca Plc has also recently entered

into an exclusive development agreement

with Moderna Therapeutics, collaboration

with Karolinska Institutet and announced

the acquisition of AlphaCore Pharma

14

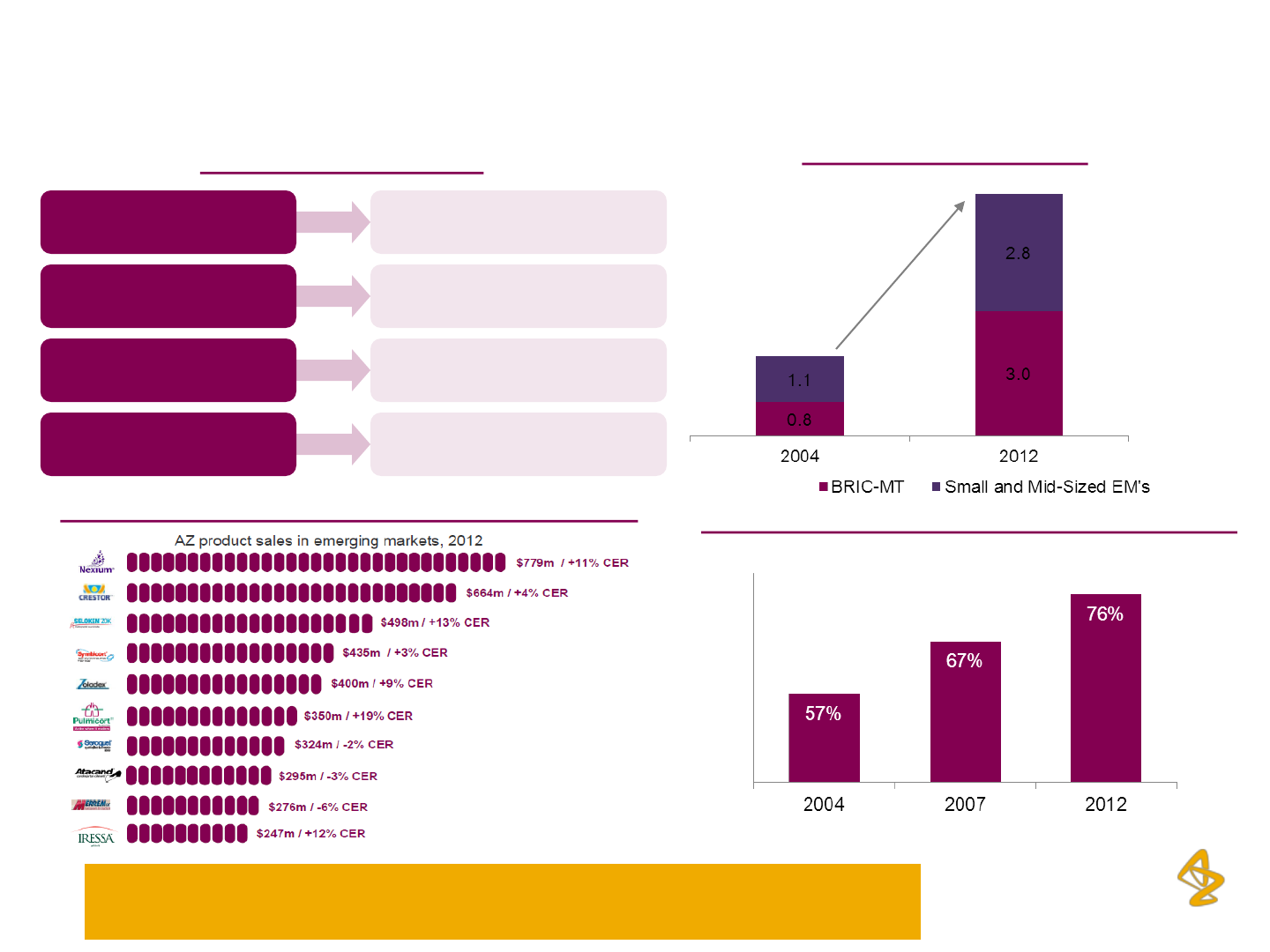

Focus on Emerging markets– A platform for

sustained growth

Emerging Markets Growth

$ Billion

$ 1.9 bn

$ 5.8 bn

Absolute

Growth

CAGR

$ 3.9 bn

$1.7 bn

$2.2 bn

15%

12%

18%

Successful Portfolio of Brands across EM’s (in $ mn)

Emerging Market Strategy

AstraZeneca is targeting high single digit growth in Emerging markets

through to 2016, with special focus on the top 15 markets, including India

Improving profitability* across emerging markets

Company’s current emerging markets margins are

similar to its Europe business 7-8 years back

*pre-R&D emerging markets operating margin (excluding central

costs), indexed to 2012 margins in established markets

Invest Early in Key

Markets

Build Share of Voice with

Best-in-Class sales force

Develop strong local

leadership

Focus on AZ products and

build BGx business

Accelerate Investment in Top

15 markets

Expand reach with multi-

channel capabilities

Transform market access,

medical affairs & affordability

Refocus on AZ portfolio &

Innovative in-licensing

Source: AstraZeneca Plc, Annual

Reports and Investor Presentations

15 15

2 AZPIL: Business Overview

Overview

16

AZPIL: Business Overview

16

FY13 Therapeutic Area-Wise Sales Contribution (%)

AZPIL is a subsidiary of AstraZeneca Pharmaceuticals AB

Sweden (89.99% shareholding), which is in turn a wholly

owned subsidiary of AstraZeneca Plc, UK, and has been

present in India since 1979, with its corporate

headquarters located in Bengaluru, Karnataka

AZPIL is present in the therapeutic areas of Cardio-

metabolism, Oncology, Respiratory & Inflammation,

Infection, Local Anesthesia and Maternal Healthcare

AZPIL’s manufacturing facilities are spread across 64

acres at Bengaluru, and commenced commercial

production in 1982

AZPIL is currently setting-up a state-of-the-art tablet

manufacturing facility with a capacity of 1.2 billion tablets

per year at a cost of Rs. 1,005 million

AZPIL has a total employee strength of ~1,588 including

dedicated sales force of ~1,166 FTEs (March 31, 2013)

AZPIL has been regularly launching products from its

global portfolio in India over the past years, leading to the

development of several domestic power brands including

Crestor, Seloken XL, Meronem, Arimidex, Zoladex,

Neksium and most recently Brilinta

Brand Therapeutic Area

Total Sales (Rs. mn)

FY 11 FY 12 FY13

Meronem Anti-Infectives

769

819

764

Linctus Codeinae Respiratory

518

489

150

Seloken XL Cardiac

317

381

386

Xylocaine Pain / Analgesics

393

377

64

Betaloc Cardiac

345

352

234

Imdur Cardiac

324

339

195

Neksium Gastro Intestinal

162

212

235

Crestor Cardiac

155

212

230

Zoladex Oncology

135

137 162

Arimidex Oncology

122

130

123

AZPIL Top 10 Brands (Based on FY12 Sales)

Cardio,37%

Respiratory,11

%

Oncology,12%

Local

Anaesthesia,4

%

Infection,28%

Maternal

Health

Care,2%

Gastro,7%

Highlighted brands have been impacted on account of the voluntary

recall initiated by AZPIL in Q4FY12

17

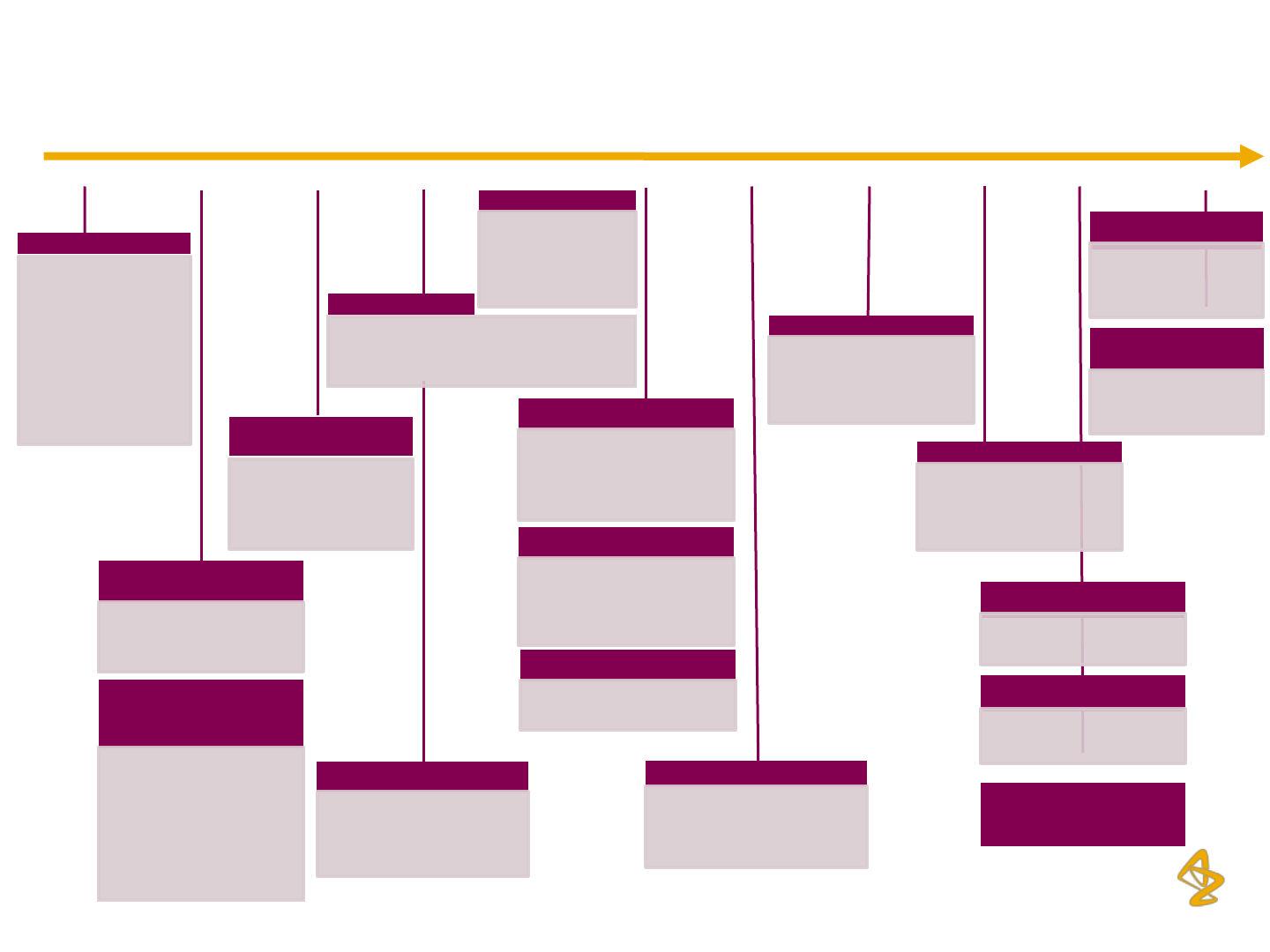

AZPIL: History & Key Milestones

17

2007 2001 2009

Start of Operations

Acquisition of majority

shareholding of AZPIL

by AstraZeneca

Pharmaceuticals AB

Sweden (AZAB)

(56.5%), following the

merger between Astra

and Zeneca

Introduction of Seloken

XL

Introduction of Seloken

XL in India from the

global portfolio

2006 2003 2002 2008

Introduction of Products

Introduced Symbicort,

(from the global portfolio)

and Gladis & Valencia

2004 2005

Open Offer for Acquisition

of further Shares

In May 2002, AZAB

increased its shareholding

to 87.21% through the first

open offer; In Dec 2002,

AZAB’s shareholding in

AZPIL reached 91.61%

through second open offer

API Facility Approval

API facility was approved by

MPA (Swedish Regulatory

Authority)

New Products

• Acquisition of Vancocin

from Eli Lily

• Launch of Partocin in

India

Introduction of Products

Introduced Faslodex & Iressa

from Global Portfolio and

Selomax & Clavatrol

Udaan Project Launched

Introduced Crestor & 7

Other Products under

Udaan Project

6 More Products Introduced

6 More Products launched

under Udaan Project

Introduction of Global

Brands

2010-11 2012

Introduction of Meronem &

Zoladex (from global

portfolio);

IT Systems

ERP system was

extended to Depots;

HRIMS system was

implemented

Awards

• No. 1 ranking in medical

rep survey

• Manufacturing excellence

award Frost & Sullivan

API Facility Approval

• Japanese FDA approval

for TBS

Brilinta

Brilinta launched in

India from the global

portfolio

Investment in New Tablet

Manufacturing Facility

Stake Reduction

Promoter reduced its stake in AZPIL from

91.61% to 89.99% over 2004 and 2005, to

comply with the local regulations

Launch of Onglyza

Launch of Kombiglyze

XR

Launch from Diabetes

Alliance Portfolio

Launch from Diabetes

Alliance Portfolio

18

AZPIL: Key Therapy Areas & Brands

18

Cardiovascular

•Brilinta^

•Onglyza*^

•Crestor^

•Seloken XL^

•Betaloc, Betaloc

H

$

•Imdur

$

•Ramace,

Ramace H

$

•Plendil

$

•Zestril

$

•Selomax

@

•Seloram

#

•Vigocil, Vigocil

M

#

•Nitract SR

•Valfect, Valfect

H

#

•Olways, Olways

H, Olways AM

#

•Kombiglyze XR*

Respiratory

•Symbicort^

•Bricanyl

$

•Mit’s Linctus

Codeinae Co

%

•Mit’s Linctus DX

%

•Bricarex,

Bricarex A

%

•Bricacef,

Bricacef PED

#

•Rhinofex

#

•Rhinomax

#

•Rhinocort

$

•Pulmicort

Respules

$

Maternal

Healthcare

•Prostodin

%

•Cerviprime

%

•Primiprost

%

•Partocin

@

•Gladis

@

•Valenzia

@

Oncology

•Zoladex ^

•Arimidex ^

•Nolvadex ^

•Iressa ^

•Casodex ^

•Faslodex ^

Infection

•Meronem^

•Vancocin CP

•Actamase

#

•Enclere

#

•Remergin

#

•Rescade

#

Neuroscience

•Diprivan^

•Xylocaine

$

•Sensorcaine

$

•Naropin

#

Gastrointestinal

•Neksium^

Leading Brands Across Therapeutic Areas

* In alliance with Bristol Myers Squibb

^ Global products introduced after 2001,

$

Global products introduced prior to 2001

#

BGx Udaan Products

%

AZPIL Local portfolio introduced prior to 2001

@

AZPIL Local products introduced after 2001 (but before Udaan Project)

Key Brand Highlights

Meronem has consistently been the No.1 brand in Carbapenems category and is

also the No. 1 Brand in the Hospital Market Segment as per IMS MAT Mar’13

Seloken XL has been the No.1 brand in the Metoprolol Once Daily market, since

last 5 years and has been growing faster than the category

Brilinta has been amongst the most successful product launches in the Indian

Pharmaceutical market, clocking sales of Rs. 51 million within 6 months of launch

Neksium has been growing faster than the gastro-intestinal therapeutic segment,

where it is present

Source: IMS Health

19

AZPIL: Manufacturing Facilities

19

Existing Formulation Facility Existing API Facility

New Tablet Manufacturing Facility -

Formulations

Capacity: 690 mn tablets

Commercial Production

Commencement : 1982

Location: Bengaluru

No. of Employees: 210

Capacity: 3600 Kgs

Commercial Production

Commencement : 1982

Location: Bengaluru

No. of Employees:37

Capacity: 1.2 billion tablets per year

Construction completed (Validation ongoing)

Location: Bengaluru

Expected Commencement of Commercial

Production: Q1FY14

AZPIL: Managing Director

Mr. Sanjay Murdeshwar

Sanjay, aged 46 years joined AZPIL as the Managing Director on May

02, 2013 and has over 17 years of diverse experience in the

Pharmaceutical Industry working across various roles and regions

with Bayer AG

Most recently, he was working as the Vice President and Head,

Commercial Operations for Bayer Healthcare – Pharmaceuticals for

Asia Pacific region. He was responsible for marketing, strategy

development, sales and marketing excellence, and business

development for the Company for Asia Pacific countries

Prior to this role, he was the Country Head – Bayer Healthcare India,

and Managing Director of Bayer Pharmaceuticals Private Limited

Previously, he has also held position for Country Head and General

Manager for Bayer Healthcare, Philippines

Graduate in Chemical Engineering from Mumbai University and has

completed Masters in Business Management from Asian Institute of

Management, Philippines

20

21

Mr. Robert Ian Haxton

Rob, aged 43 years joined AZPIL as the Whole Time Director and Vice

President – India Operations on February 01, 2013 and has over 20

years of diverse experience in the Pharmaceutical Industry working

across various roles and regions with AstraZeneca

Most recently, he was working as the Head of Regional External

Supply (EMEA), for AstraZeneca Plc. He managed a multicultural and

multi geographic team located in UK, Turkey, Russia, South Africa,

Egypt and Israel. He developed the 5 year category strategy for the

EMEA contractor supply base

Prior to this role, he was Supplier Account Manager – Global External

Sourcing, and Product Supply Chain Manager with AstraZeneca Plc

Previously, he has also been Plant Manager in factories across the

AstraZeneca Global network

Graduate (BSc. Hons) in Biomedical Technology from Sheffield

Hallam University

AZPIL: Whole Time Director & VP – India Operations

22

Mr. Justin Ooi

Non-Executive Director

Mr. Justin Ooi, aged 42 years has completed post graduate qualification at MGSM (Australia) and executive

programes at INSEAD and London Business School.

He has over 25 years of experience. He has been with AstraZeneca for over 19 years and has gained

comprehensive experience across both commercial and financial functions - with the last 10 years being part

of the Senior Executive Team. He is currently the Area Finance Director for AstraZeneca International Region

(including Asia and India). Prior to this role, he has held various senior level positions including Area Finance

Director for AstraZeneca Asia Pacific Region, and Sales & Marketing Director and Chief Financial Officer for

AstraZeneca Australia.

AZPIL: Non-Executive Directors (AZ Group)

Mr. Ian Brimicombe

Non-Executive Director

Mr. Ian Brimicombe aged 49 years, is a graduate from King’s College, London. He has exposure on audit, tax

and corporate finance at Coopers & Lybrand, London (now PricewaterhouseCoopers) from 1986, qualifying as

a Chartered Accountant and a Chartered Tax Adviser.

He has been with AstraZeneca since 1994 and has held various senior positions in Corporate Finance and

Taxation. From 2001, he has been Director of Group Tax, responsible for global tax operations and delivery of

AstraZeneca's group tax targets. Currently, he is the Vice President – Corporate Finance for AstraZeneca Plc.

He has been on the Board of AZPIL since September 2006

23

Mr. D. E. Udwadia, Chairman

Independent Director

Mr. K. S. Shah

Independent Director

Mr. D E Udwadia, aged 73 years, holds Degree in BA (Hons) and LLB and also holds Master’s Degree in

Political Science and History. He has over 48 years of active corporate law practice and wide-ranging

professional experience. He is an Advocate and a Solicitor by profession. He is a Solicitor and Advocate of

the Bombay High Court and a Solicitor of the Supreme Court of England. He is a Senior Partner of M/s.

Udwadia, Udeshi & Argus Partners, a reputed law firm.

Mr. Udwadia has been on the Board of AZPIL from inception and since September 2000, as Chairman of the

Board. He is also on the Board of several other reputed companies.

Mr. K S Shah, aged 72 years, is a Graduate in Commerce and a Fellow Member of the Institute of Chartered

Accountants and a Fellow Member of the Institute of Company Secretaries of India.

He has rich experience in industry including general management and administration. Prior to his appointment

in the Company, he was the Finance Director and Deputy Managing Director of May & Baker (I) Ltd. He has

been on the Board of AZPIL since November 2001, and was the Managing Director of Astra IDL from July

1988 to September 1991. He is also Chairman of the Audit Committee of the Board.

AZPIL: Independent Directors

Mr. Narayan K Seshadri

Independent Director

Narayan K Seshadri aged 56 years, is a Chartered Accountant by profession with over thirty years of

professional experience.

He is the founder of Tranzmute Capital & Management Private Limited. Earlier, he had founded Halcyon

Resources & Management that had partnered with a US investment management group. Prior to establishing

Halcyon, he was the Managing Partner at KPMG’s Business Advisory Services Practice and was also a

member on Andersen’s global CEO advisory council. He holds Board positions in many companies. He has

been on the Board of AZPIL since December 2012.

AZPIL: Key Event Update

In Q4FY12, AZPIL initiated a voluntary recall of twelve products following AZ

Worldwide Audit Group’s (WWAG) quality audit, on account of which it faced supply

issues in FY13, which are currently in the final stages of being remediated

24

Voluntary Recall initiated in

Q4FY12

• Voluntary recall was initiated for

twelve products manufactured at

Bengaluru plant, following the

AstraZeneca Worldwide Audit

Group’s (WWAG) quality audit

• As a precautionary measure,

production was also voluntarily &

temporarily suspended to review

manufacturing & quality practices

at the plant, and undertake

remedial measures

• This resulted in further impact on

other non-recalled products as

well, and led to losses in FY13

Remedial Measures

• 54 experienced personnel from

AstraZeneca Global were

seconded to India on short as well

as longer term assignments to

help address these manufacturing

/ quality issues

• Site Investment with Managerial,

leadership, process and

equipment changes

• Comprehensive training plan

delivered

• Recruitment of diploma level

education shop floor workmen

Present Situation

• Key impacted products like

Xylocaine (Injection), Prostodin,

Seloken XL and Sensorcaine

have already been re-introduced

in the market

• The manufacturing of the non

tablet impacted products has

been outsourced to select

contract manufacturers in India

• Efforts are in place to reintroduce

the remaining impacted products

and re-establish AZPIL’s market

position

25

AZPIL: Non-Impacted Brands continue to deliver

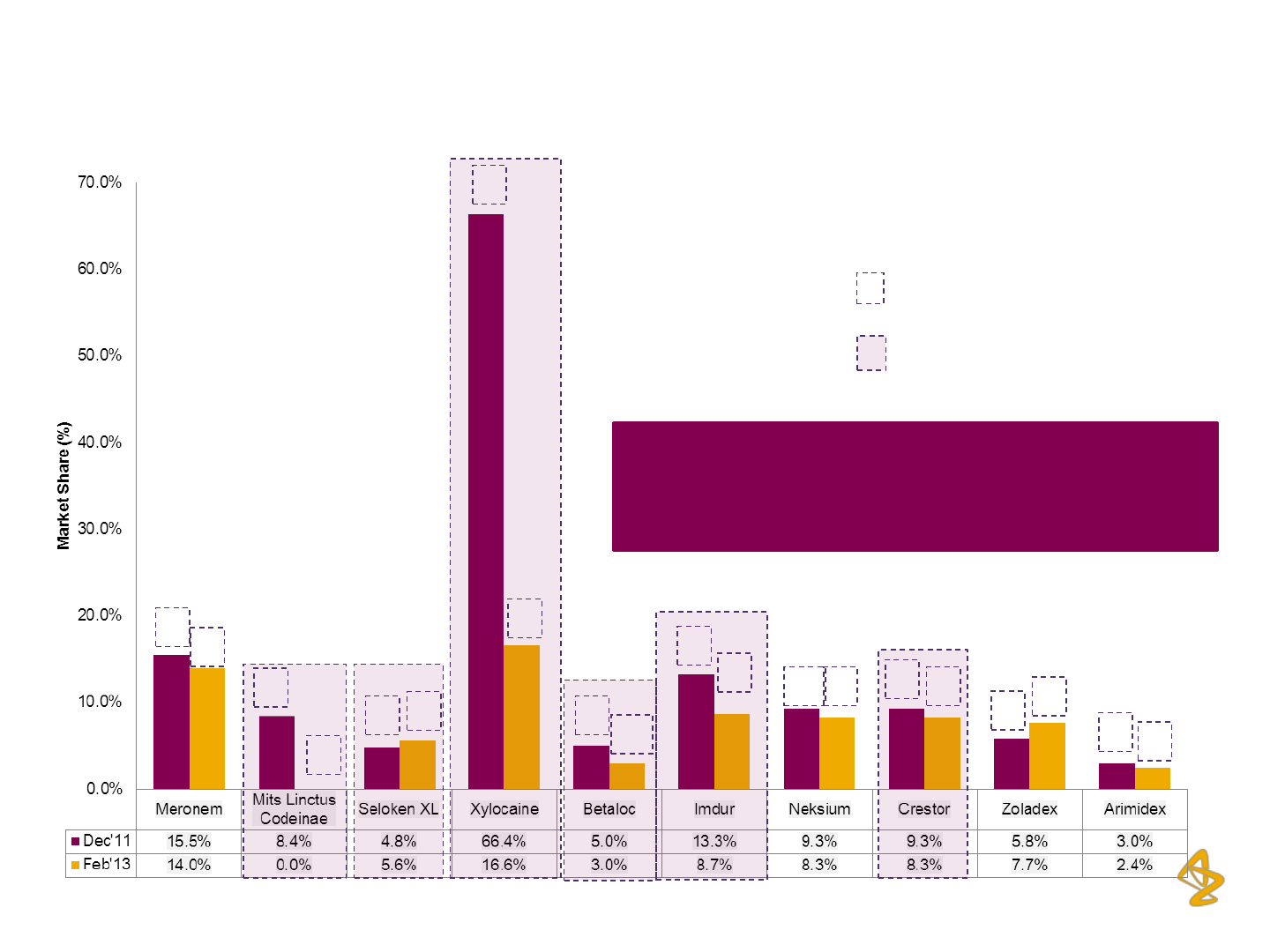

Resilient Performance

Source: IMS Health

*Market Share based on MAT Values

Brand-wise Market Share

*

and Ranking

(Top 10 Brands)

1

1

3

6

3

3

1

2

2

10

2

3

11 9

3

3

4

3

6

9

Ranking

Brands Impacted due to Recall

6 out of the top 10 AZPIL brands rank amongst

the top 3 in their respective therapeutic

categories

26

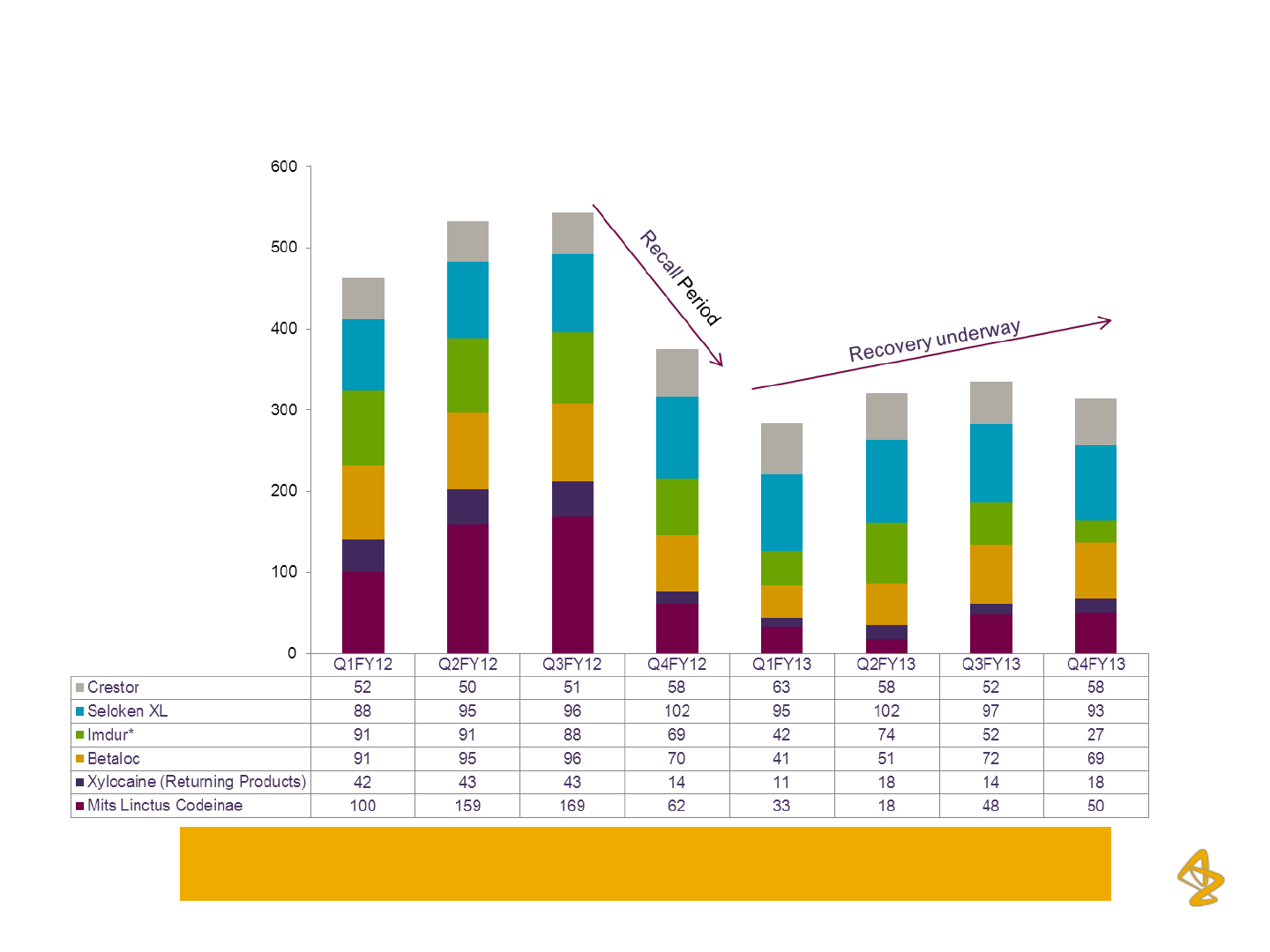

AZPIL: Steady Recovery Under-way

Sales for Impacted Brands (In Rs. million)

Remediation of Supply Issues enabling recovery across Key Impacted Brands

*Imdur sales were impacted between Q2FY13 and Q4FY13 on account of certain supply issues, which are currently being remediated

Products representing 8 – 10% of the revenues are being discontinued in the

current financial year (FY14)

15%

24%

24%

30%

29%

32%

34%

24%

18%

7%

-14%

7%

14%

13%

18%

18%

20%

20%

14%

11%

4%

-22%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12 FY13

EBITDA Margin PAT Margin

1,401

1,808

1,965

2,329

2,774

3,136

3,681

4,024

6,003

5,379

4,009

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12 FY13

217

432

481

700

807

1,012

1,261

946

1,098

366

-580

-1,000

-500

0

500

1,000

1,500

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12 FY13

104

245

258

431

487

615

738

576

641

198

-895

-1,000

-800

-600

-400

-200

0

200

400

600

800

1,000

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12 FY13

27

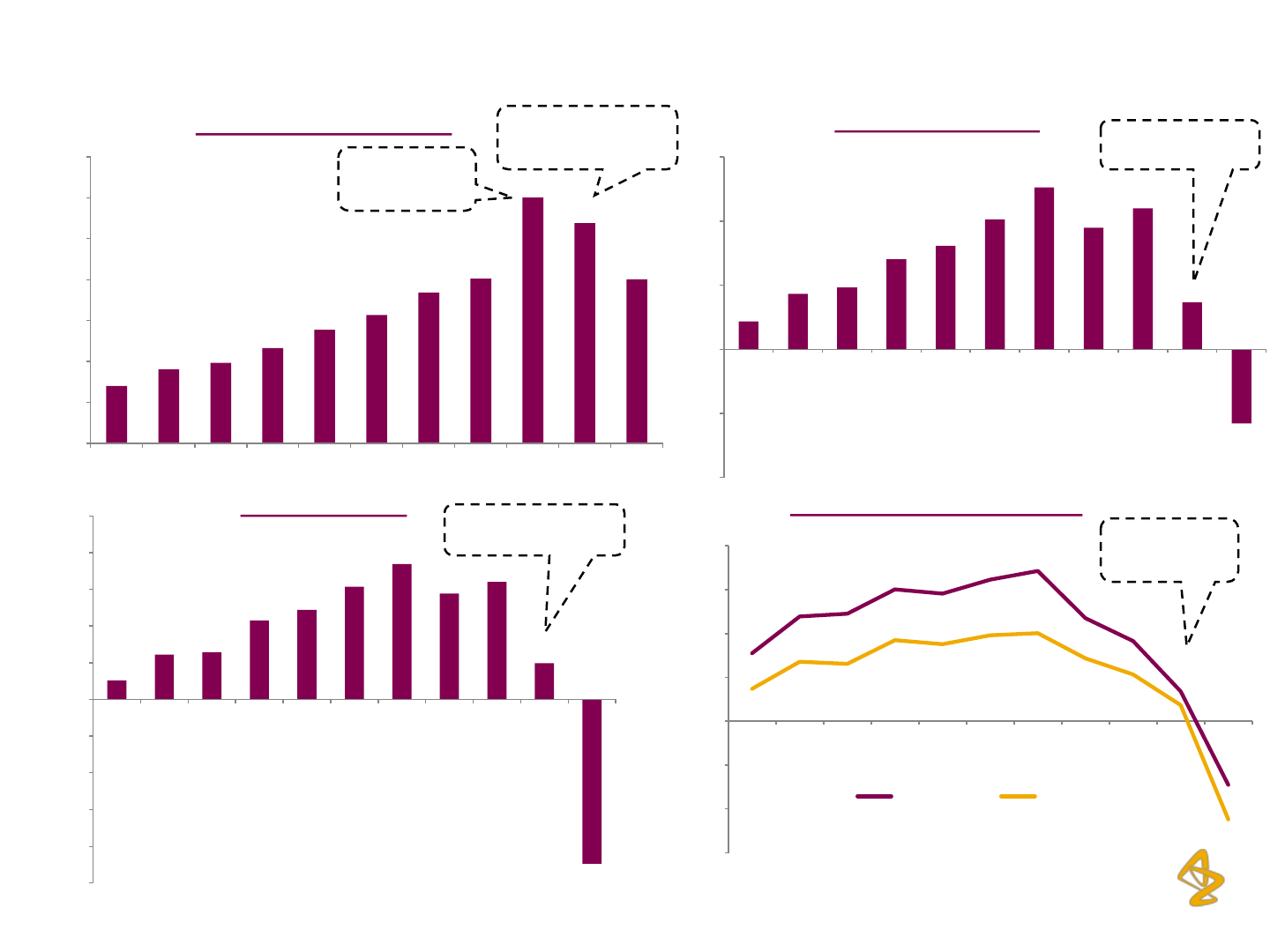

AZPIL: Financial Overview

27

Total Income (Rs. million)

EBITDA (Rs. million)

EBITDA and PAT Margins (%)

PAT (Rs. million)

Voluntary recall

initiated

2002-11 CAGR 22.1%

Voluntary

recall initiated

2002-11 CAGR 19.1%

15 month

period FY11

2002-11 CAGR 16.7%

Voluntary recall

initiated

Voluntary

recall

initiated

28

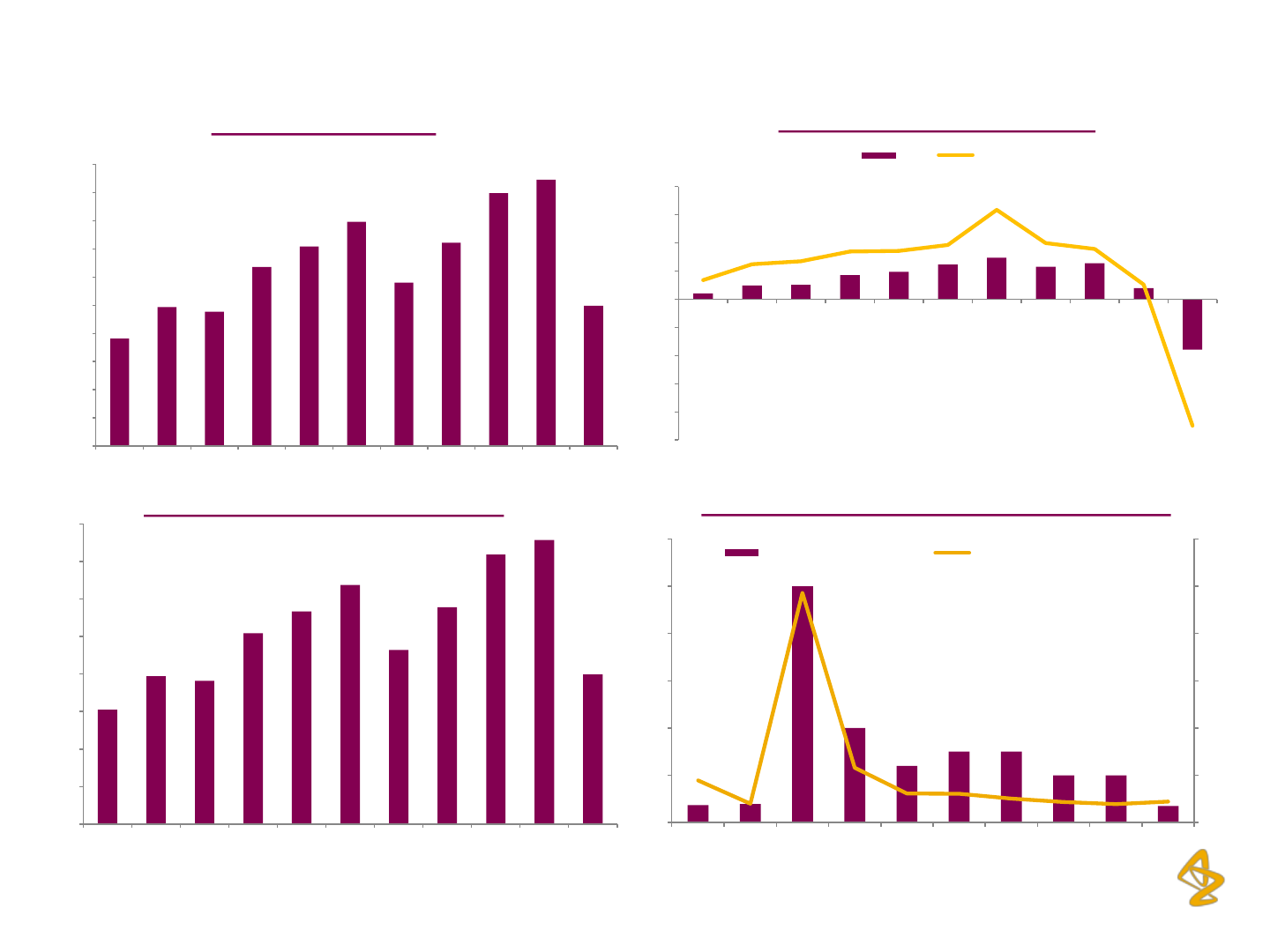

Net worth (Rs. million)

EPS (Rs.) / Return on Net worth

Dividend Per Share/ Dividend Payout Ratio (%)

Book Value Per Share (BVPS in Rs.)

3.7

3.9

50

20

12

15 15

10 10

3.5

89

40

485

116

62

61

51

43

39

44

0

100

200

300

400

500

600

0

10

20

30

40

50

60

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12

Dividend Per Share (INR) Dividend Payout Ratio- RHS (%)

AZPIL: Financial Overview

762

987

955

1,272

1,417

1,593

1,162

1,445

1,797

1,893

998

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12 FY13

4

10

10

17

19

25

30

23

26

8

-36

14

25

27

34

34

39

64

40

36

10

-90

-100

-80

-60

-40

-20

0

20

40

60

80

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12 FY13

EPS RoNW

30

39

38

51

57

64

46

58

72

76

40

0

10

20

30

40

50

60

70

80

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12 FY13

29 29

3 AZPIL: Key Highlights

Overview

30

AZPIL: Key Investment Highlights

30

Leveraging Global Strength

Outstanding Parent profile providing

significant technical & financial backing;

Consistent product launches from Parent’s

portfolio

Significant Growth Levers

Favorably positioned to benefit from India’s

fast growing Pharma market

Re-focused for Delivery

Resolution of Supply Issues in India and

taking steps towards its strengthening

position in the Indian Market

Strong Pipeline Potential

Significant launches planned in India from

global portfolio and partnerships.

High Corporate Governance

Standards

High corporate governance;

Passion for quality and patient safety ,

demonstrated by initiating voluntary recall

based on findings of AstraZeneca Worldwide

Audit Group’s (WWAG) quality audit

Long Term Commitment to India

Among the first MNCs to establish India

presence; Focus on India in-line with Global

strategy to ramp-up business in emerging

markets

31 31

AZPIL: Leveraging Global Strength

Product launches from Parent’s portfolio

2002 2003 2004 2005 2006 2007 2008 2009 FY11 FY12 FY13

Cardiovascular

Crestor Brilinta

Respiratory

Symbicort

Turbuhaler

Antibiotic/

Infection

Meronem

Relaunch

of Diprivan

Oncology

Zoladex

Arimidex

Zoladex

(10.8 mg)

Casodex

Faslodex

Relaunch

of

Nolvadex

Iressa

Anaesthesia

Diprivan

Maternal

Healthcare

Gastro Intestinal

Neksium

Diabetes

Alliance

Onglyza

Kombiglyze

XR

32 32

Robust Global Pipeline

AZD2014

moxetumo

mab* AZD4547 MEDI-551* lesinurad

brodalumab

*

volitinib*

MEDI0639

* Olaparib

#

tremelimum

ab

fostamati

nib* metreleptin*

AZD1208

MEDI3617

*

selumetinib

* MEDI-573*

naloxegol

*

AZD9150 MEDI-565* AZD5069

benralizum

ab* CAZ AVI*

AZD8330*

MEDI6469

* AZD2115*

mavrilimum

ab*

AZD5363*

MEDI4736

* AZD5423* MEDI8968*

AZD8848* MEDI4212 AZD1722*

sifalimuma

b*

AZD7594*

MEDI2070

* AZD6765 MEDI-546*

AZD7624

MEDI9929

* AZD5213

Tralokinum

ab

AZD1446*

MEDI5872

* AZD3241 MEDI7183*

AZD3293* MEDI5117 AZD5847

ATM AVI MEDI-557

MEDI-559

MEDI-550

Oncology

Respiratory &

Inflammation

CVMD

Neuroscience

Infection

Legend

Phase I

26 NMEs

Phase II

21 NMEs

Phase III/

Registration

6 NMEs

AZPIL: Strong Pipeline Potential

Significant technical support and robust Global Pipeline & launches

from collaborations offers significant future growth visibility

World Class R&D and Technology Support

Investment >$4 billion each year

9,800 Employees

Spread across 10 principal R&D centers in 6 countries

Collaborated with different companies including Bristol-Myers

Squibb & Amgen and acquisitions like Ardea Biosciences,

MedImmune & Amylin Pharmaceuticals (in alliance with BMS),

which has further augmented current R&D pipeline, with

approximately 40% being sourced externally

Launched five of its global blockbuster products in the Indian

Market

Access to global technical knowledge and Product portfolio

R&D Support

Technology

Support

#

Decision to accelerate

Olaparib to Phase III,

and committed to EU

filing in 2013

33

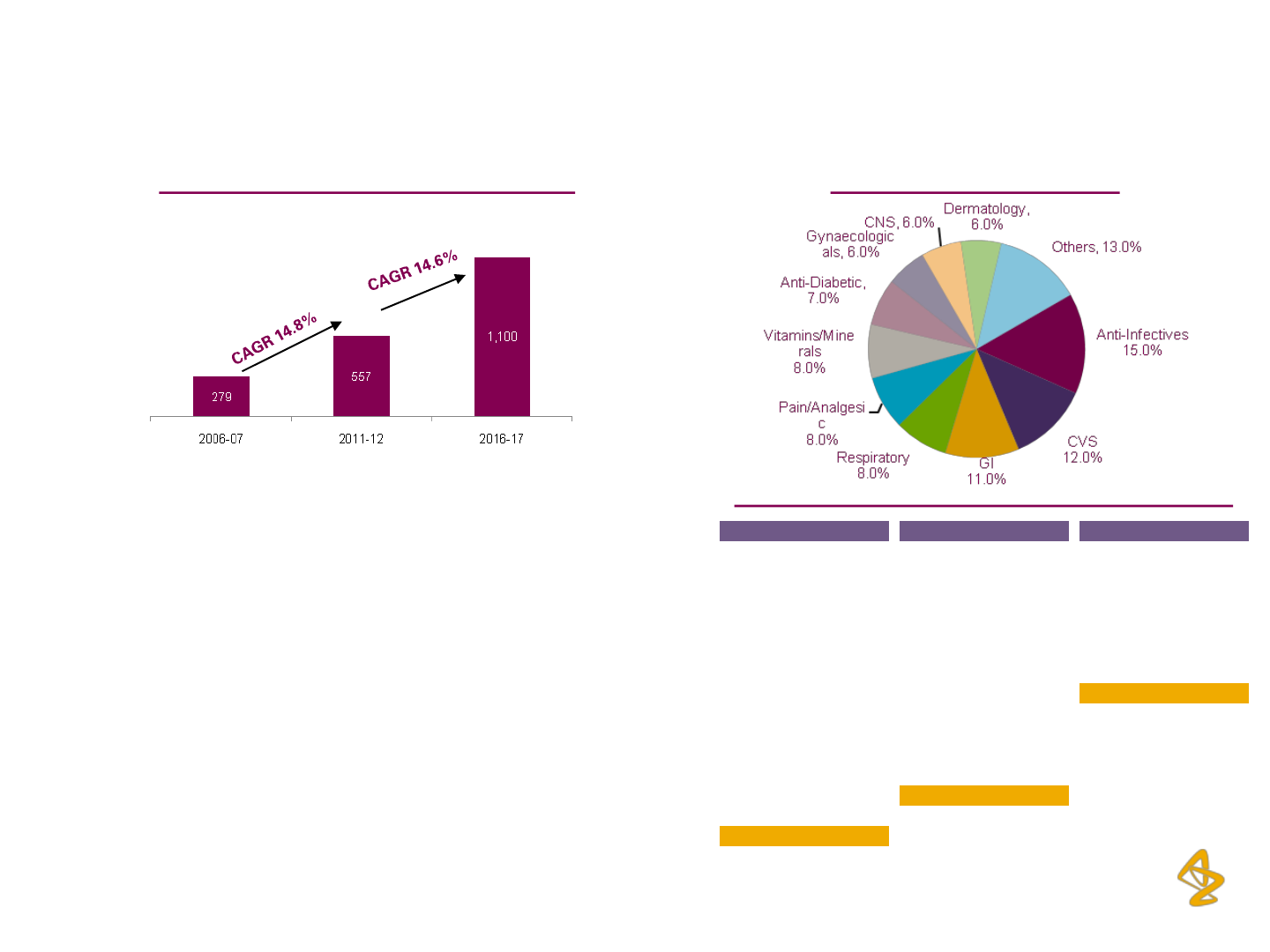

Domestic Formulations Market (in Rs. Bn) Split by therapeutic segment

Source: Industry Research

Expected CAGR of 14 - 17% over the next 5 years with

the market size expected to cross Rs. 1 trillion

High growth expected in Specialty therapies (Diabetes,

Oncology, CVS, CNS, among others); Mass therapies

such as anti-Infective and Gastro segments also

expected to continue growing steadily

Top 10 therapies have remained constant over the last 5

years, consistently contributing more than 85% of the

market in value terms

2006 Rankings

1 United States

2 Japan

3 France

4 Germany

5 China

6 Italy

7 Spain

8 UK

9 Canada

10 Brazil

11 Australia

12 Mexico

13 South Korea

14 Russia

15 India

India’s improving ranking in Global Pharma Space

2011 Rankings

1 United States

2 Japan

3 China

4 Germany

5 France

6 Brazil

7 Italy

8 Spain

9 Canada

10 UK

11 Russia

12 Australia

13 India

14 South Korea

15 Mexico

2016 Rankings

1 United States

2 China

3 Japan

4 Brazil

5 Germany

6 France

7 Italy

8 India

9 Russia

10 Canada

11 UK

12 Spain

13 Australia

14 Argentina

15 South Korea

Ranking in all years based on spending in constant US$ at Q4

2011 exchange rates

Source: IMS Market Prognosis, May 2012

AZPIL: Significant Growth Levers

Favorably positioned to benefit from India’s fast growing Pharma Market

34

Household incomes* to drive healthcare spending Rising prevalence of several chronic diseases

Expanding healthcare delivery market Growing health insurance market

Source: HealthCare Market Research

AZPIL: Significant Growth Levers

Favorably positioned to benefit from India’s fast growing Pharma Market

Percent of Population

* Annual income

35

Favorable product mix of AZPIL

Catering to majority segments of the Indian Pharma Market

AZPIL: Significant Growth Levers

Favorably positioned to benefit from India’s fast growing Pharma Market

Though traditionally, acute therapies have dominated the Indian pharma market, holding a significantly higher share

than chronic segments, but with changing lifestyles and demographics, the disease profile of the Indian population is

shifting towards chronic ailments, leading to faster growth in chronic segment (CAGR of 17-19% over FY09-12 as

compared to the CAGR of 11-14% recorded by the acute segment during the same period)

AZPIL’s portfolio is favorably positioned to capture this re-alignment in the Indian Pharma market from acute

therapies to chronic therapies, over the long term

AZPIL is also considering select marketing tie-ups for some of the products, in order to improve their market

penetration and revenues

0% 20% 40% 60% 80% 100%

Sanofi India

Astrazeneca India

Abbott India

IPM

Novartis India

Pfizer India

Wyeth India

Glaxo India

Acute Chronic

Therapeutic Segments

(Rs. billion) 2006-07 2011-12E 2016-17P

Anti Diabetic 12.4 36.5 80 – 87

Anti Infectives 49.7 91.3 147 – 161

CVS 28.2 66.7 128 – 140

Dermatology 15.5 31.0 62 – 68

Gastro Intestinal 30.5 59.2 109 – 119

Gynaecologicals 15.2 31.5 58 – 61

Neuro / CNS 15.0 31.4 63 – 69

Pain / Analgesics 26.3 46.4 82 – 89

Respiratory 25.8 47.3 83 – 91

Vitamins / Minerals 23.8 44.4 85 – 93

Others 36.4 70.9 125 – 137

Total 279.0 556.6 1050 – 1100

Source: Industry Research; E – Estimated; P – Projected; Therapeutic segments

where AZPIL has presence have been highlighted

36

AZPIL: High Corporate Governance Standards

Emphasis on consistent global standards of sales and marketing practices

Maintaining a strong focus on patient safety

Exploring ways of increasing access to healthcare for more people, tailored locally to different

patient needs

High Operating

Values & Ethics

AZPIL’s Board has historically been composed of non-executive and independent directors, with

the promoter representative directors forming the rest

AZPIL’s Chairman is a Non-Executive and Independent director, Mr. D. E. Udwadia, who is an M.A

L.L.B. (Hons.) by qualification and has over 48 years of active corporate law practice and wide-

ranging professional experience; He is a solicitor and advocate of the Bombay High Court, and

solicitor of the Supreme Court of England, and brings with him significant legal expertise

Robust Board

Composition

Stringent and superior global quality and manufacturing standards

Undertook a voluntary recall of sterile products manufactured at its Bengaluru plant, following

AstraZeneca Worldwide Audit Group’s (WWAG) quality audit in Q4FY12

As a precautionary measure, also voluntarily suspended production temporarily to review

manufacturing and quality practices at the plant, and undertake remedial measures

Resulted in near-term adverse financial impact, but was done in the overall interests of the Indian

consumers and doctor fraternity, in line with its global best practices

Upholds High Corporate Governance standards of the AstraZeneca Group

Voluntary Recall

upholds Global

Quality and

Corporate

Governance

Standards

AZPIL: Re-focused for Delivery

Re-Focused to deliver products and performance

37

To launch products suitable for the Indian market from its global portfolio and alliance partners,

which shall augment the existing product portfolio

Launching Global

Products in India

State of the art manufacturing facility being established in Bengaluru, Karnataka with capacity to

manufacture 1.2 billion tablets, expected to commence operations from Q1FY2014

Commencement of

New Tablet Facility

Reintroduction of

products

Manufacturing of injectables and liquids are being outsourced by AZPIL to selected contract

manufacturers in India

Outsourcing

Prior to the recall, AZPIL was one of the fastest growing MNC pharma companies in India

On account of the recall, AZPIL faced certain supply issues in FY2013, which are in the process of

being remediated and addressed, with key products like Xylocaine (Injection), Prostodin, Seloken

XL and Sensorcaine already being re-introduced in the market

AZPIL: Re-focused for Delivery

Re-alignment of Manufacturing Strategy

Existing Formulations Manufacturing Facility

Tablet Manufacturing Facility

The new tablet manufacturing facility is expected to commence commercial production in Q1FY2014

As on March 31, 2013, Rs. 737 million has been incurred towards the manufacturing facility, and an additional Rs.

80 million is proposed to be incurred before commencement of commercial production

Further, additional investment of Rs. 188 million has been approved towards the manufacturing facility, which

shall be spent over FY14-FY15

API Facility

Agreement with AZAB Sweden for supply of TBS over the next three years

38

The existing manufacturing facility is proposed to be closed by end FY14, once the new tablet manufacturing

facility commences production, the technology transfer of products is completed and the production stabilizes

This would allow us to consolidate our operations leaving approximately 30 acres of land unutilized

39

AZPIL: Long-Term Commitment to India

In-line with the Global Emerging Market Strategy

39

Establishing New state-of-the-art manufacturing facility with an investment of Rs 1,005 million

Significant Human capital investment as well, in terms of bringing experienced personnel within

the group to manage the commencement and stabilization of the new manufacturing facility

Voluntary non-repayable financial grant by the promoter AstraZeneca Pharmaceuticals AB

Sweden of approximately USD 22.5 mio (Rs. 1,192 mio) to USD 26.5 mio (Rs. 1,404 mio) over the

three years period FY14 – FY16 under a subvention agreement, of which the first tranche of USD

14 mio (Rs. 740 mio) shall be provided to the company in the current financial year FY14

Investment

Commitment

India remains a key strategic growth market for the AZ group, among the emerging markets

Finds mention as one of the fastest growing markets for the Group

Presents significant potential in terms of AZ’s diabetes alliance product portfolio, on

account of the significant diabetic population

Strategic Growth

Market for AZ

Global

Present in India for more than 34 years

Existing formulations manufacturing facility commenced commercial production in 1982 and has

been supplying products for the Indian and global markets for more than 30 years

Among the earliest MNC pharma companies to enter the Indian market

Long-standing

presence in India

The voluntary recall initiated by AZPIL is indicative of AstraZeneca group’s commitment to

providing high quality medicines, and ensuring patient safety, while demonstrating its long term

commitment to the Indian market

Voluntary recall

Initiative

AZPIL: Going Forward

40

Company’s revenues to grow ahead of market over this period

Re-establish its market position in the impacted products portfolio

Return to profitability in the current financial year and deliver PBT margin in

high teens from the next financial year

The above should be read together with the underlying assumptions given in slide 41

National Pharmaceuticals Pricing Policy (NPPP), if implemented could have

an adverse impact of 10 – 15% to the sales of AZPIL

AZPIL: Assumptions Underlying Way Forward

Strong performance of key AZPIL brands and products

Remediation Strategy remains on track without any further supply issues, both in-house and from

outsourcing suppliers

Ability to overcome any resistance in re-establishing the impacted products back in market

No delay in new product launches on account of regulatory approvals / any other reasons

Restructuring exercise completed smoothly within estimated timelines and budgeted costs

Commencement of new tablet manufacturing facility along expected timelines and within the

estimated costs, and stabilization of the facility in line with current plans

Internal Factors

and Business

Environment

No Adverse impact of any other macro-economic & Industry / Company specific developments

and any unforeseen circumstance

General Risk

The Indian Pharma market continues to grow in double digits over the next 2-3 years

There are no adverse changes in the proposed NPPP (incremental), Patent product pricing,

Pharma Marketing Policy, Patent Act or significant shift in government view on Product Patents

There are no adverse changes in Government policies on import of medicines in bulk or tablet

form and those on clinical trials or associated compensation rules

There are no adverse changes in custom or import duties

The Government continues to provide an un-interrupted supply of Codeinae

There is no adverse impact of generic entry in the patented products space

Industry Outlook

and Regulatory

Environment

41

Thank You

{kind=link}